The last two years have been unprecedented, in many ways. 2020 witnessed the deepest, but shortest recession in recorded history; 2021 saw an unusual, uneven recovery in which supply struggled to keep up with demand.

We’ll enter the new year with the vestiges of the pandemic economy still with us. Normalcy has yet to be regained; more likely, it is being redefined. The following transitions will be critical to performance in 2022:

The first of these is the transition from zero tolerance to learning to live with COVID-19. Since early 2020, the course of the pandemic has determined the course of the global economy and economic policy, and may continue to do so. Happily, COVID-19 is in something of a retreat at the moment, but a cursory reading of the history reveals that viruses of this kind rarely sit still. Vaccination has advanced, but is far from complete.

Given its proven ability to travel with relative ease, COVID-19 anywhere is a threat everywhere. Societies will have to remain vigilant, but will have to accept some level of risk as the price for sustaining commerce.

The second transition surrounds de-globalization. The past two years have illustrated that supply chains are far more brittle than we may have suspected. The pandemic also highlighted the immense dependence that Western nations have on output from China and Southeast Asia. The desire for additional resilience and economic security will drive some production closer to home.

A movement away from unfettered globalization seems well underway; the question is: how far will it go? As the world’s economic geography shifts, so will the fortunes of nations. That could produce challenges for debt sustainability and corporate profits, among other things.

The difficult relationship between the United States and China will contribute to economic disengagement. Each accuses the other of slights and transgressions that range from minor to much more serious. Each expects, and in some cases demands, allegiance from other countries, who find themselves caught uncomfortably in the middle.

Ultimately, some level of collaboration between China and the United States will produce the best results for the global economy, and for global society. Almost everyone has a stake in the competition between Washington and Beijing, which can have no clear winner.

Policy retreat lies ahead. Fiscal and monetary policy moved with both size and speed to address the challenges presented by the pandemic. With the global recovery still not fully complete, calibrating the retreat from crisis-era measures will be no less challenging. Pulling back prematurely could leave permanent scars; staying too generous for too long could overstimulate. Most economies will be facing fiscal headwinds in the year ahead.

Monetary policy has certainly done its part; to some, it has done more than enough. Inflation has been running well ahead of targeted levels; assessing how it will fare over the longer run is very difficult. Risks to inflation are skewed to the upside; we therefore expect an expanding community of central banks to move away from balance sheet growth and the zero lower bound in 2022. Appropriately previewed and formulated, the retreat should not come at a great cost to market performance.

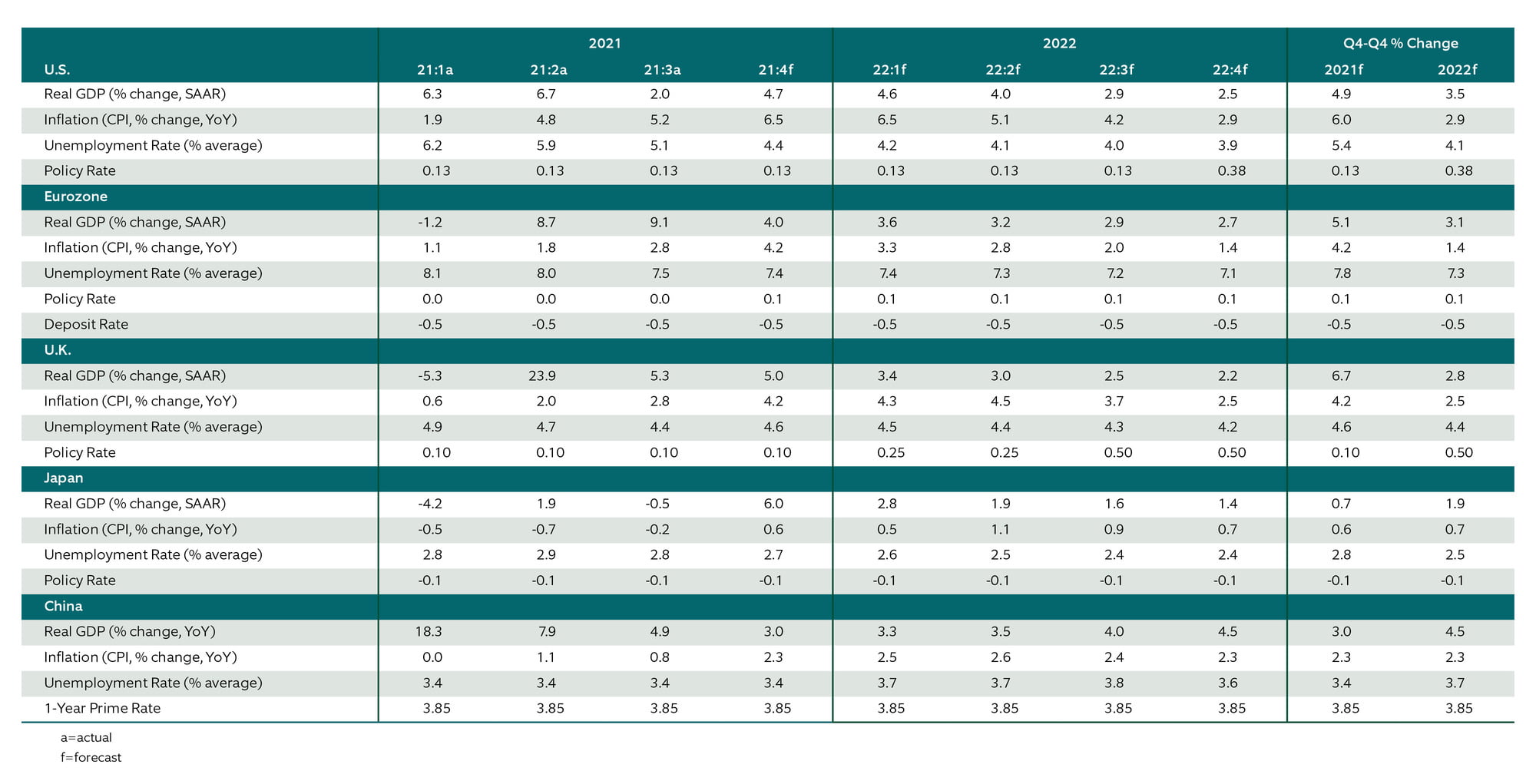

Click on the chart to zoom in and explore the data.

The final transition surrounds the drive to digitize. The pandemic led more of us to do more things more often virtually, accelerating movement down the adoption curve that is unlikely to reverse. The resulting boost to automation and e-commerce is changing cost and pricing structures in ways that we are only beginning to comprehend.

"Technology is certainly changing the nature of work and the skills required to do it."

Technology is certainly changing the nature of work and the skills required to do it. In a digitizing world, those with more modest levels of education will face rockier paths to prosperity. If policy fails to address the disparity, support for economic systems may come under increasing question.

Following are discussions of our outlook for individual markets, with emphasis on how these four transitions will affect them.

Watch the video of our economic experts as they address entering the new year with the vestiges of the pandemic economy and the transitions critical to performance in 2022.

Discover the latest economic insights from our chief economist on social media.