As you reinvest your time and money to grow your business, it is equally important at this stage to set the foundation for building and sustaining your long-term wealth.

Items at the top of your priority list should include setting up the optimal entity structure for your company, putting in place an estate plan for your assets, and identifying sources of liquidity to fund your personal expenses and financial goals.

The entity structure of your business will have significant implications for how you grow your business and your wealth over the long run. Successful entrepreneurs periodically reevaluate their choice of corporate entity (e.g., limited liability company vs. S corporation) and how those entities relate (e.g., holding companies and management companies). They also remain flexible to modify these structures as their business becomes more complex and as tax laws change.

Consider the following factors when building the optimal entity structure for your business:

Individual and corporate tax implications, including the ability to qualify as “qualified small business stock”

Ability to raise capital and accumulate cash on balance sheet

Placing hard assets (e.g., real estate) and soft assets (e.g., operating business) in separate corporate entities to limit liability and facilitate transfers of assets out of your estate

How business decisions will be made (e.g., a corporate board versus a general partner)

Ease of converting to a different corporate entity (e.g., from a C corporation to an S corporation) in response to anticipated tax law changes

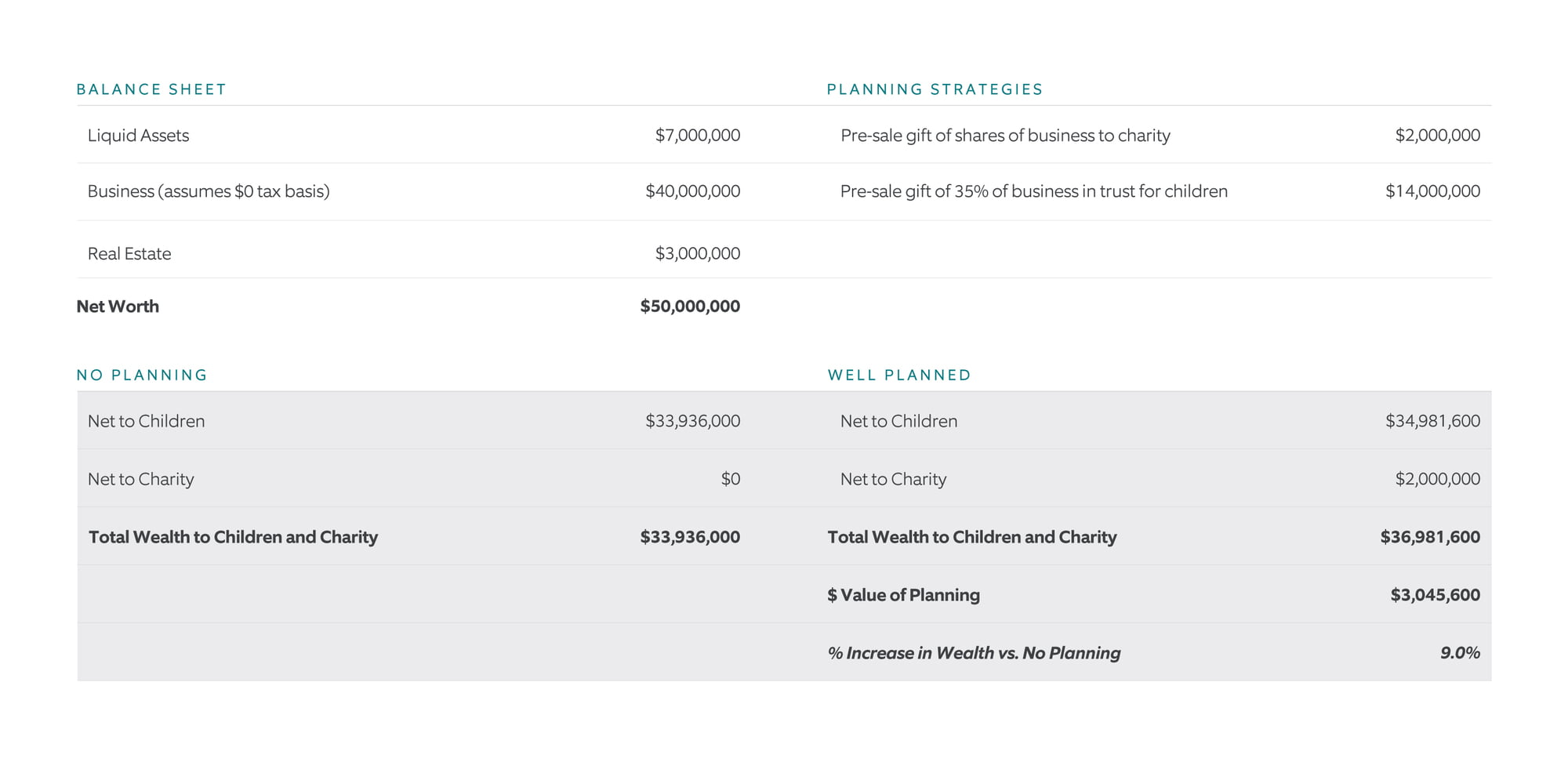

For most entrepreneurs knee-deep in building their business, estate planning may not be top of mind. Implementing the right estate plan early on, however, can result in significant tax savings down the road when you exit your business. To the extent you can transfer some of the value of your business out of your estate now (e.g., into trusts for charity or your family), any increase in value from the time you transfer shares out of your estate up to the time of sale may pass to your beneficiaries free of estate and gift taxes.

Questions to ask when building your estate plan include:

Keep in mind, transferring shares outside of your estate does not necessarily mean giving up control of your business. Many entrepreneurs, for example, will convert a portion of their business’ shares into “non-voting” shares and transfer those shares out of their estate, while retaining voting shares. In the example on the following page, we show the value of one such instance.

Example assumes entrepreneur sells their business for $40 million and applies a 35% valuation discount on the value of the shares transferred to trusts for their children. Assumes a 40% estate tax rate and federal estate tax exemption of $12.06 million per individual (assumes entrepreneur is married).

Entrepreneurs are typically hyper-focused on finding capital to help grow their business. However, it is equally important to have access to near-term liquidity for personal expenses (e.g., funding education, buying a second home) as your business grows so you can reinvest profits back into your company.

Take a comprehensive “personal cost of capital” approach and evaluate all potential liquidity sources that may be available, including:

Consider how each potential capital source stacks up across the following factors: